Asda Stores Ltd CL-2012000299 and Others v MasterCard Incorporated and Others

| Jurisdiction | England & Wales |

| Judge | The Hon. Mr Justice Popplewell,Mr Justice Popplewell |

| Judgment Date | 30 January 2017 |

| Neutral Citation | [2017] EWHC 93 (Comm) |

| Docket Number | CL-2012-000299, 000344, 000355, 000553 to 000556, 000727, 000767, 000858, 000959 and 000960 |

| Court | Queen's Bench Division (Commercial Court) |

| Date | 30 January 2017 |

[2017] EWHC 93 (Comm)

The Hon. Mr Justice Popplewell

CL-2012-000299, 000344, 000355, 000553 to 000556, 000727, 000767, 000858, 000959 and 000960

IN THE HIGH COURT OF JUSTICE

QUEEN'S BENCH DIVISION

COMMERCIAL COURT

Royal Courts of Justice, Rolls Building

Fetter Lane, London, EC4A 1NL

Paul Lowenstein QC, Fergus Randolph QC, Christopher Brown, Max Schaefer and Hannah Glover (instructed by Stewarts Law LLP) for the Claimants

Mark Hoskins QC, Matthew Cook and Hugo Leith (instructed by Jones Day) for the Defendants

Hearing dates: 13–16, 20–23, 27–30 June, 4–7, 21 July, 28 September, 10–13 October 2016

Approved Judgment

I direct that pursuant to CPR PD 39A para 6.1 no official shorthand note shall be taken of this Judgment and that copies of this version as handed down may be treated as authentic.

Introduction

The Defendants are collectively referred to in this judgment as MasterCard; it is not necessary to distinguish between them for the purposes of the issues which I have to decide. MasterCard sets the level of fees to be charged for its credit and debit card transactions. Such fees are known as multilateral interchange fees or "MIFs". The MIFs are (indirectly) paid by the merchants with whom cardholders use their cards to purchase goods or services. Although MasterCard sets the MIFs, it does not receive them; the MIFs are paid to the institutions which issue the payment cards to cardholders. The issuers are typically, but by no means exclusively, banks. The Claimants are well known high street retailers who collectively claim to have paid a total of about £437 million by way of MIFs in the relevant period (broadly speaking since 2006). The central issue in these cases is whether the MIFs set by MasterCard for credit and debit card transactions by consumers in the relevant period, and in the relevant territories (UK, Ireland and cross border transactions between EEA countries), are tortiously anti-competitive in breach of UK, Irish and EU competition law; and if so by how much.

There are twelve separate actions, two of which have been brought to an end by settlement since the commencement of the hearing. The trial before me was to determine a number of issues which were selected and framed to determine all issues of liability and some issues affecting quantum (if relevant), in what was referred to as "the Phase 1 trial". Other questions relevant to quantum have been left for consideration (if appropriate) at a subsequent hearing ("the Phase 2 trial").

Background to the dispute

In this section I address the background under the following headings:

(1) The MasterCard scheme.

(2) Types of cards and users.

(3) The legal framework for the claims.

(4) The regulatory history.

(5) The CAT decision.

(6) An overview of the MasterCard MIFs and the markets.

(7) MasterCard Projects: Forward, Alhambra and Porsche.

(8) The witnesses.

(1) The MasterCard scheme

The MasterCard payment card scheme, like that of Visa, is often described as a "four-party" scheme, although it involves five parties. It is to be distinguished from "three-party" schemes which involve three parties.

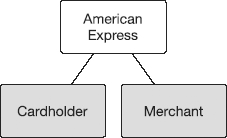

A three-party scheme is represented diagrammatically as follows:

The operator of a three-party scheme deals directly with cardholders and merchants. It issues the cards to cardholders, who pay it a fee. It also charges the merchant a fee. Payments are cleared through the operator: the cardholder uses his card to buy goods or services from the merchant; the merchant is paid by the operator the price less the merchant fee; the operator recovers the full price of the goods or services from the cardholder, typically having provided credit. As the diagram suggests, the leading example of a three-party scheme in the UK is American Express ("Amex"). Another smaller three party scheme is operated by Diners Club.

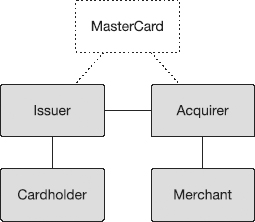

By contrast, a "four-party" scheme involves five parties in the following structure:

The four parties in grey in the diagram are each necessarily involved in the flow of payments arising from a transaction: the issuer issues the payment card to the cardholder; the cardholder "pays" for the goods or services provided by the merchant by card; the acquirer provides the "acquiring" service to the merchant which allows it to receive card payments, and pays the merchant for the goods and services, less a discount. The acquirer obtains payment from the issuer, who charges the cardholder for the transaction. MasterCard charges a fee to both issuers and acquirers for their ability to participate in the scheme.

The financial dynamics for those participating in the scheme are as follows:

(1) When the cardholder purchases goods or services from the merchant, he does not immediately make any payment. In the case of a credit card he does not have to pay the issuer until the end of the period of credit agreed with the issuer. Typically in the UK he will receive free credit until the end of the month. In the case of a debit card, the debit from his account is swift but not instantaneous because it is made by the issuer in response to clearing via the acquirer.

(2) Following a sale, the merchant recovers the price from the acquirer, who services the payment. The acquirer charges a merchant service charge ("MSC") for the service which is deducted from the price paid to the merchant.

(3) The acquirer recovers his outlay, plus a profit, from the issuer; the issuer does not pay the acquirer the full price of the goods or services, but deducts an amount by way of interchange fee.

(4) The issuer charges the full value of the transaction to its cardholder customer. In theory therefore the issuer recovers in full from the customer and earns potentially profit making revenue in the form of (a) any fees charged to the cardholder for the issue or use of the card (b) the interchange fee and (c) any profit on the interest rate charged to the customer for credit. In practice there falls to be set against such potential profit (a) the costs of issuing cards and processing recovery from the customer (b) the cost of benefits or rewards offered to cardholders which attach to the use of particular cards in particular ways (c) the cost of free credit for the interest free period and (d) losses due to cardholder default or fraud, which under the terms of the scheme fall on the issuers rather than the merchants or acquirers.

(5) MasterCard has a contractual relationship with both the issuers and acquirers, who are licenced to participate in the scheme and undertake to abide by a single set of scheme rules set by MasterCard. These are detailed and prescriptive, and updated from time to time. The scheme rules in force at 28 May 2015 ("the Scheme Rules") were treated by the parties as representative of those in force throughout the relevant period for the purposes of the dispute in this case, and references in this judgment are to the relevant parts of that edition. MasterCard's income is derived from the fees it charges to issuers and acquirers in return for licencing their use of the cards.

Interchange fees can in theory be agreed bilaterally between issuers and acquirers. In practice this is not how the interchange fee is determined. Under the Scheme Rules (Rule 8.3), MasterCard sets the interchange fees which are to apply compulsorily in default of bilateral agreements. These are the multilateral interchange fees or "MIFs". In practice there are no material bilateral agreements, and so the MIF always applies. This is not surprising: in a putative bilateral negotiation between an issuer and an acquirer the issuer has no incentive to accept less than the default MIF and the acquirer no incentive to offer more.

Not only have the MIFs set by MasterCard varied over the period covered by the claims, but at any given time MasterCard has had a wide variety of different MIFs for different categories of transaction. There are distinctions between territories and between credit and debit card transactions, so that the broadest relevant categories are the card-type/territory groups that define the MIFs in issue in this claim: i.e., EEA debit, EEA credit, UK debit, UK credit, Irish debit and Irish credit MIFs. But within such groups (in the territories in issue and elsewhere) MasterCard also differentiated MIFs according to a variety of different factors, such as whether the transaction was face-to-face, online, or made by mail or telephone order; whether the card and/or the payment terminal had chip and pin functionality; how the payment was verified; whether cards were premium cards; and by the category of merchant.

MIFs may be expressed as a percentage of transaction value, sometimes referred to as " ad valorem", as a fixed sum per transaction, or as a combination of both. Very broadly speaking, MasterCard's debit card MIFs have tended to be set on a fixed or combined basis, and its credit card MIFs have been purely ad valorem.

The payment flows between...

To continue reading

Request your trial

-

Britned Development Ltd v ABB AB

...have been in if he had not sustained the wrong for which he is now getting his compensation or reparation”. 11McGregor at [10–046]. 12 [2017] EWHC 93 (Comm) at 13 Day 1/p.49. 14Asda at [306(1)]. 15 Asda at [306(2)]. 16 C(2013) 3440; Asda at [306[3)]. 17 Following: Rimer J in SPE Internation......

-

Abanka D.D v Abanca Corporación Bancaria S.A.

...most apparently straightforward credit or debit card payment transaction (see Asda Stores Ld & Ors v Mastercard Incorporated & Ors [2017] EWHC 93 (Comm) (30 January 2017) at [4]–[22] for a summary of the complex and diverse nature of what is going on in such payment schemes, reflected also......

-

Fludrocortisone acetate tablets: anti-competitive agreement (50455)

...Racecourse Association v OFT [2005] CAT 29, paragraphs 132 and 133; see also by analogy ASDA (and others) v MasterCard (and others) [2017] EWHC 93 (Comm), paragraph 45; Article 101(3) Guidelines, see paragraphs 51 to 58; Guidelines on Vertical Restraints OJ 2010/C130/01, paragraph 47; secti......

- Mastercard Incorporated and Others v Merricks

-

Interchange Fees - Returns Or Recoveries?

...of household name retailers sought to recover £437 million in interchange fees from MasterCard (Asda Stores Ltd v MasterCard Inc [2017] EWHC 93 (Comm). In a key departure from Sainsbury's allegations, Asda et al claimed that interchange fees at any level were The Court decided that MasterCa......

-

Sainsbury's v Visa: Court Of Appeal Set To Get MIFfed

...Ltd v Visa Services LLC, Visa Europe Ltd and Visa UK ltd. [2017] EWHC 3046 (Comm) 2 Arcadia & Ors v MasterCard & Ors [2017] EWHC 93 (Comm) 3 Sainsbury's Supermarkets Ltd v MasterCard Incorporated and Others [2016] CAT The content of this article is intended to provide a general guid......

-

Cross-border litigation: Evaluating the Brexit impact – a socio-legal model for data analysis

...[2011] EWCA Civ. 2.99. (UK) Sainsbury’s Supermarkets Ltd v. MasterCard Inc, [2016] CAT 11; Asda Stores Ltd & others v. MasterCard Inc,[2017] EWHC 93 (Comm); Walter Hugh Merricks CBE v MasterCard Inc, [2017] CAT 16; Sainsbury’s SupermarketsLtd v. Visa Europe Services LLC, [2017] EWHC 3047 (C......