F.S. Securities, Ltd v Commissioners of Inland Revenue

| Jurisdiction | England & Wales |

| Judgment Date | 04 June 1964 |

| Date | 04 June 1964 |

| Court | Chancery Division |

HIGH COURT OF JUSTICE (CHANCERY DIVISION)-

COURT OF APPEAL-

HOUSE OF LORDS-

Surtax - Undistributed income of company - Dividends received on securities dealt in by company - Whether company an investment company - Income Tax Act, 1952 (15 & 16 Geo. VI & 1 Eliz. II, c. 10), Sections 245 and 257(2).

The Appellant Company was incorporated in August, 1954, and was at all material times under the control of not more than five persons. Its memorandum of association provided, inter alia, that it might purchase, hold and deal in shares, etc.

In December, 1954, and March, 1955, the Company purchased the entire share capital of three companies, each of which had substantial undistributed profits. On 28th March, 1955, all three companies declared large dividends. The value of their shares decreased as a result, and this decrease was reflected in the trading account of the Company for the period from 1st September, 1954, to 31st March, 1955. The Company claimed and was allowed relief under Section 341, Income Tax Act, 1952, in respect of a trading loss for that period on the basis that the dividends should be excluded in computing its trading profit or loss for tax purposes.

On 22nd January, 1960, a direction under Section 245, Income Tax Act, 1952, was given in respect of the Company's actual income from all sources for the above-mentioned period, on the footing that it was an investment company within the meaning of Section 257(2). On appeal, the direction was confirmed by the Special Commissioners.

In the Court of Appeal and the House of Lords, the Company contended that the dividends declared on 28th March, 1955, were, consistently with Cenlon Finance Co., Ltd. v. Ellwood, 40 T.C. 176, trading receipts to be taken into account in arriving at its liability under Case I of Schedule D.

Held, that the Commissioners' decision was correct.

Stated under the Income Tax Act, 1952, Section 247(1) and Section 64, by the Commissioners for the Special Purposes of the Income Tax Acts for the opinion of the High Court of Justice.

1. At a meeting of the Commissioners for the Special Purposes of the Income Tax Acts (hereinafter referred to as "the Special Commissioners")

held on 17th November, 1960, and thence adjourned to 18th November, 1960, 31st January, 1st February and 20th March, 1961, F. S. Securities, Ltd. (hereinafter called "the Appellant"), appealed against a direction made by the Special Commissioners on 22nd January, 1960, on the footing that the Appellant was an investment company within the meaning of Section 257(2), Income Tax Act, 1952, to which the provisions of Section 245, Income Tax Act, 1952, applied, directing that for the purposes of assessment to Surtax the actual income of the Appellant from all sources for the period 1st September, 1954, to 31st March, 1955, should be deemed to be the income of the members of the Appellant. The grounds of the appeal were that the Appellant was not an investment company within the meaning of the said Section 257(2), Income Tax Act, 1952, and therefore the direction of the Special Commissioners was incorrect in law and ought to be discharged.2. Evidence was given at the hearing of the appeal by Leonard Lever (hereinafter referred to as "Mr. Lever") a director of the Appellant from 1954 to 1959; May Lever (hereinafter referred to as "Mrs. Lever") the wife of Mr. Lever; Leslie Lavy (hereinafter referred to as "Mr. Lavy") a chartered accountant and a partner in the firm of Lavy Ascher & Co., chartered accountants, and a director of the Appellant from 1954 to 1959; and the following documents were produced and admitted or proved:

(i) Statutory declaration dated 13th May, 1949, made by Raymond George Harding Banbridge.

(ii) Memorandum and articles of association of the Appellant.

(iii) Settlement dated 1st January, 1955, between Reuben Lipman, Rita Lavy and Mr. Lavy.

(iv) Trading and profit and loss account of the Appellant for the period 1st September, 1954, to 31st March, 1955, and balance sheet at that date.

(v) A bundle of schedules comprising: (a) purchases and sales of securities and dividends received by the Appellant from 1st September, 1954, to 31st March, 1955, (b) interest and dividends received by the Appellant, and (c) securities held by the Appellant on 31st March, 1955.

(vi) Direction dated 22nd January, 1960, issued to the Appellant by the Special Commissioners.

(vii) Notice of apportionment dated 22nd January, 1960, issued to the Appellant by the Special Commissioners.

(viii) Notice of assessment to Surtax 1954-55 dated 22nd January, 1960, made on Mr. Lever by the Special Commissioners.

(ix) Notice of charge dated 22nd February, 1960, issued to the Appellant by the Special Commissioners.

(x) A bundle of accounts of the trustees of A. D. and P. J. Lever covering the period 1st April, 1953, to 5th June, 1960.

(xi) A bundle of accounts of the Lavy (children) trust covering the period 1st January, 1955, to 31st March, 1957.

(xii) Agreement dated 20th March, 1956, between Eastlandia, Ltd., Mr. Lever, Mrs. Lever, Mr. Lavy, and Rita Lavy.

(xiii) Minute book of the Appellant.

(xiv) Profit and loss account of the Appellant for the year to 31st March, 1956, and balance sheet at that date.

(xv) A letter dated 1st February, 1949, from J. H. Jarman to Mr. Lever.

(xvi) A bundle of correspondence.

(xvii) Income and expenditure account of Lavy (children) trust for the year to 31st March, 1958, and balance sheet at that date.

The above documents are not attached to and do not form part of this Case, except to the extent that they have been incorporated herein.

3. We found the following facts admitted or proved on the evidence adduced at the hearing of the appeal:

-

(2) The Appellant was incorporated on 19th August, 1954, with a share capital of £100 divided into 100 shares of £1 each, which were held as follows during the relevant period:

Mr. Lever and Mrs. Lever as trustees (as from 19th October, 1954.)

83

Mr. Lavy and Mrs. Lavy as trustees (as from 18th January, 1955.)

15

J. H. Howard (transferred to Mr. and Mrs. Lever, 4th February, 1955.)

1

J. D. Collinson (transferred to Mr. and Mrs. Lever, 4th February, 1955.)

1

(3) The directors of the Appellant were Mr. Lever, Mr. Lavy and Mr. Yablon, and the Appellant carried on the business of a finance company.

(4) The memorandum of association of the Appellant contained, inter alia, the following objects for which the Appellant was established:

To carry on the business or businesses of Stock and Share Dealers, and to purchase, subscribe for, acquire, hold and deal in shares, stocks, debentures, bonds, securities and obligations generally of any government, company, corporation or body; and to promote finance, advance money on hire purchase or otherwise assist any company or companies, whether corporate or unincorporate, or persons as may be thought fit; and to act as agents for the issue and placing of, and to underwrite shares, debentures and other securities or obligations.

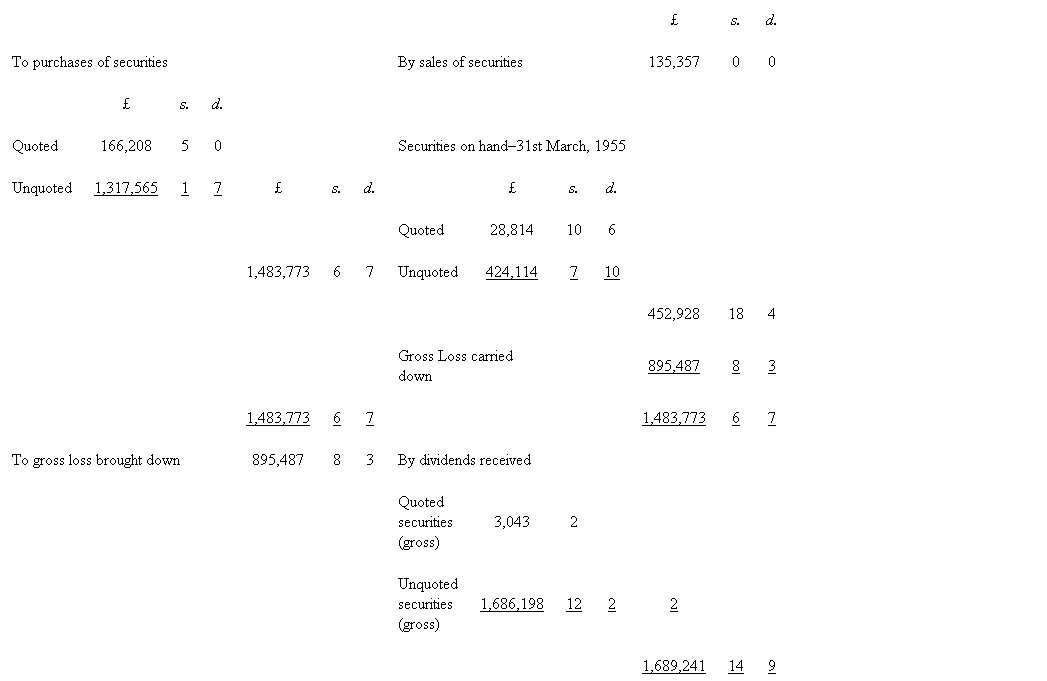

(5) The trading and profit and loss accounts of the Appellant for the period 1st September, 1954, to 31st March, 1955, contained, inter alia, the following entries:

(6) Trading and profit and loss account for the period 1st September, 1954, to 31st March, 1955

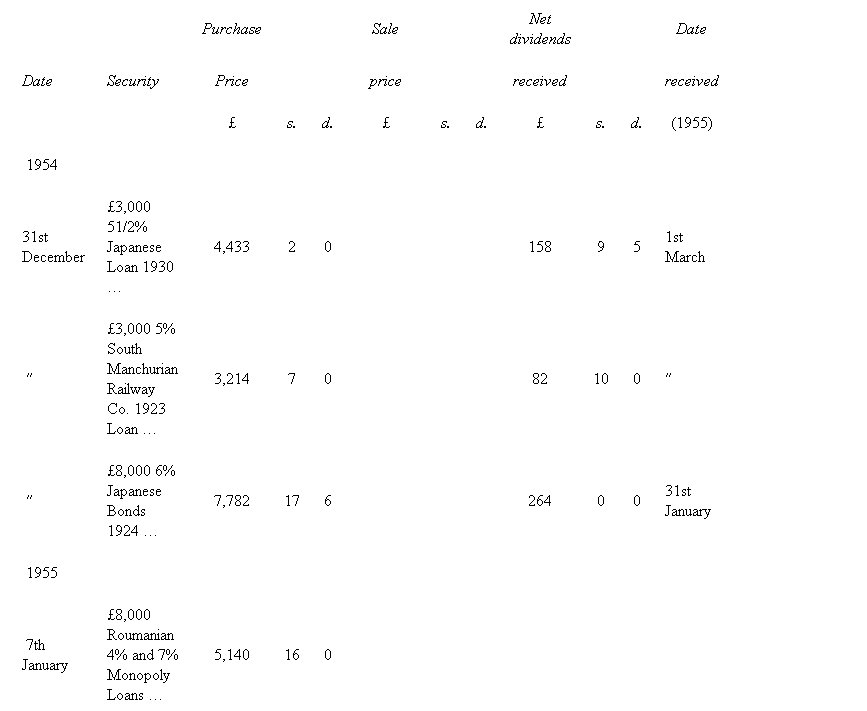

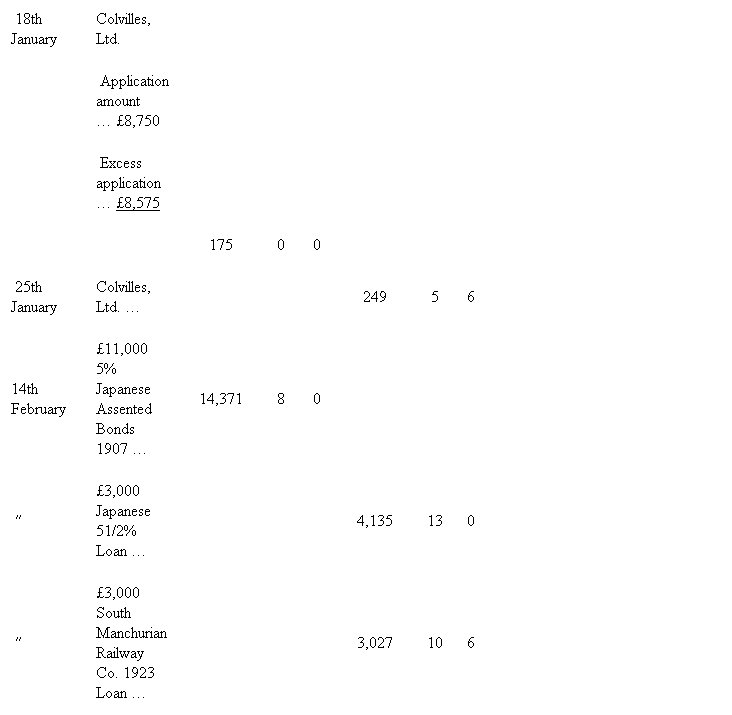

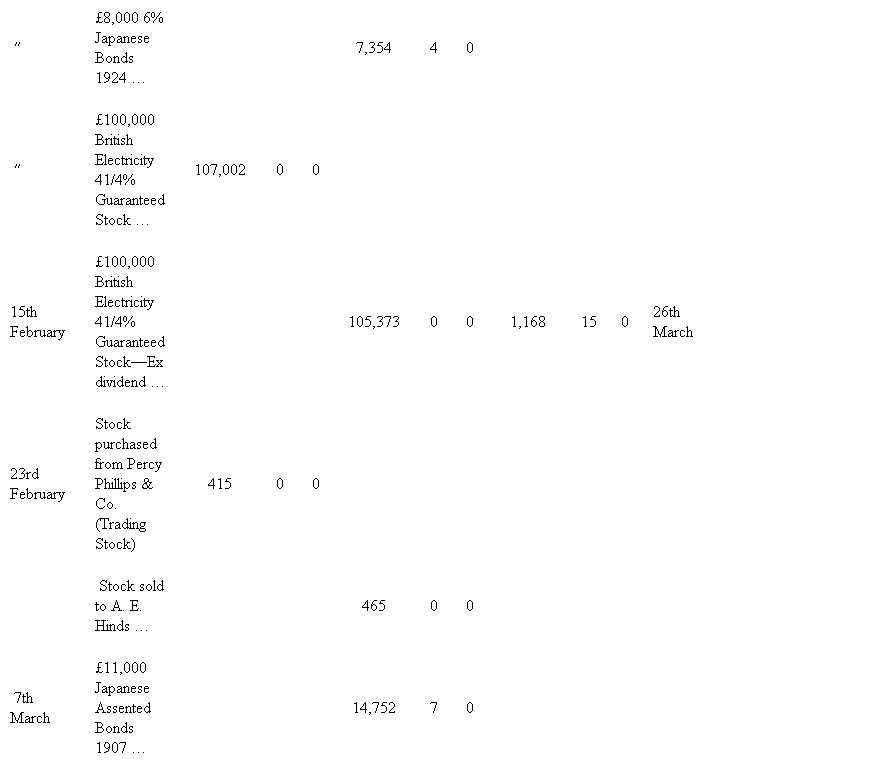

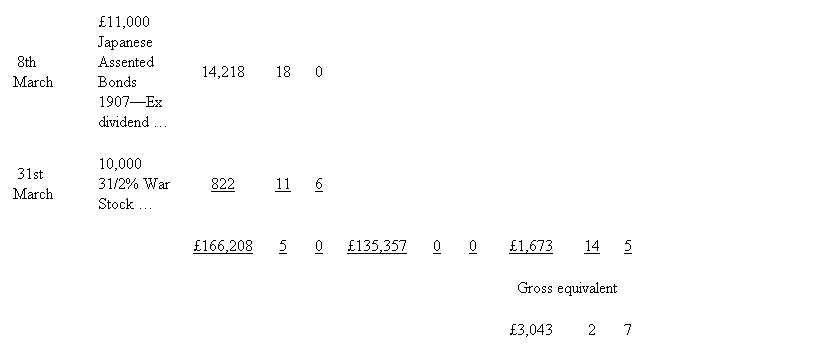

(7) The figures for purchases and sales, dividends received and securities on hand at 31st March, 1955, in respect of quoted securities were made up as follows:

(8) Purchases and sales of securities and dividends received for the period 1st September, 1954 to 31st March, 1955

(10) Quoted securities on hand at 31st March, 1955

£ |

s. |

d. |

|||

£11,000 Japanese 5% 1907 Assented Bonds |

… |

… |

14,218 |

18 |

0 |

£1,000 Roumanian External Loan |

… |

… |

665 |

0 |

0 |

£7,000 Roumanian 7% Monopolies |

… |

… |

4475 |

16 |

0 |

£1,000 British Land Co., Ltd. |

… |

… |

822 |

11 |

6 |

£10,000 31/2% War Stock |

… |

… |

8,632 |

5 |

0 |

£28,814 |

10 |

6 |

(11) The figure of £1,317,565 for purchases of unquoted investments represented the cost to the Appellant of the undermentioned purchases of the entire share capital of three companies, i.e.:

(12) 10th December, 1954, B. & Co., Wool Merchants (Bradford), Ltd. £175,075;

(13) 3rd March, 1955, Cranwell (Holdings) Ltd. £732,823;

(14) and, 25th March, 1955, N.E.T. Holdings, Ltd. £409,667.

(15) To purchase these shares the Appellant arranged overdraft facilities with its bankers who agreed to, and did in fact, lend the Company 93 per cent. of the value of the shares which were lodged with them by way of security. As additional security the bank also took a charge over the cash assets of those companies the whole of whose shares were acquired by the Appellant. The assets of these three companies consisted almost entirely of liquid resources and each had substantial undistributed profits. The object of the directors of the Appellant in purchasing these shares was to carry out an operation colloquially known as "dividend-stripping", that is to say, to transfer to the Appellant by way of dividend the maximum amount of the undistributed profits of these companies, and then to use the resulting fall in the value of the shares of these companies as the basis of a loss claim under Section 341, Income Tax Act, 1952, so as to reclaim the tax deducted or deemed to have been deducted from the dividends declared and paid to the Appellant. These operations were duly carried out by the Appellant for each of the three companies mentioned above, and the dividends paid to the Appellant on 28th March, 1955, were as follows:

B. & Co. Wool Merchants (Bradford), Ltd. (net) |

£33,523 |

Cranwell (Holdings), Ltd. (net) |

£494,629 |

N.E.T. Holdings, Ltd. (net) |

£399,256 |

Total |

£927,408 (£1,686,198 gross) |

(16) The shares of the three "stripped" companies were retained by the Appellant for any ultimate purpose that the directors could put them to, their market value at 31st March, 1955, being estimated as follows:

B. & Co. Wool Merchants (Bradford)... |

To continue reading

Request your trial

-

Ian Douglas Thomson (HM Inspector of Taxes) (Respondent) Gurneville Securities Ltd (Appellants)

... ... In The Supreme Court of Judicature Court of Appeal (Revenue Paper) (On Appeal from the Chancery Division, Mr. Justice Goff) ... P.W. MEDD, and Mr. J.P.F. WARNER (instructed by The Solicitor of Inland Revenue) appeared on behalf of the Respondent ... LORD ... are recited at length in the case stated by the Special Commissioners, which exhibits all the relevant documents. It is, therefore, only ... ...