Kelsall Parsons & Company v Commissioners of Inland Revenue

| Jurisdiction | Scotland |

| Judgment Date | 06 January 1938 |

| Date | 06 January 1938 |

| Docket Number | No. 19. |

| Court | Court of Session (Inner House - First Division) |

1ST DIVISION.

RevenueIncome taxProfitsCapital or incomeSum paid as compensation for termination of agency agreementAgency terminated one year before natural expiry of agreementIncome Tax Act, 1918 (8 and 9 Geo. V, cap. 40), Sched. D, 1 (a) (ii).

A firm of manufacturers' agents held for many years an agreement constituting them the sole selling agents in Scotland of an English company. In terms of the agreement the firm were entitled to receive a percentage on the value of all orders received from Scotland, the minimum sum payable to them annually being fixed at 2000. The agreement was more than once renewed, and in September 1932 it was continued for three years from 30th September 1932. During the later years of the agreement the firm held about eleven agencies for various manufacturers, and their gross receipts averaged about 4000 annually, including the fixed minimum payment of 2000 from the English company. In 1934, at the request of the English company, it was agreed that the agency agreement should be terminated on 30th September 1934, being one year prior to its natural expiry. The English company paid the firm the sum of 1500 as compensation for the termination of their agreement before its natural expiry.

The firm contended that this sum of 1500 was not chargeable to income tax, on the ground that it was a capital payment made as compensation for the disorganisation of the structure of their business.

Held that the sum was chargeable to income tax, in respect that it was really paid as compensation for loss of profits during the last year of the agency agreement.

Observed that a different decision might have been reached if the agreement had had a considerable period still to run.

At a meeting of the Commissioners for the General Purposes of the Income Tax Acts for the Division of the Lower Ward of the County of Lanark, Messrs Kelsall Parsons & Company appealed against an assessment made on them under Schedule D of the Income Tax Act, 1918, for the year ending on 5th April 1937 in

respect of the profits of their trade or business,1 based on their profits for the trading year ending on 30th September 1935, on the ground that, in computing their profits, a sum of 1500 received by them from George Ellison, Limited, should not be taken into accountThe General Commissioners refused the appeal, and, at the request of the appellants, stated a case for appeal to the Court of Session.

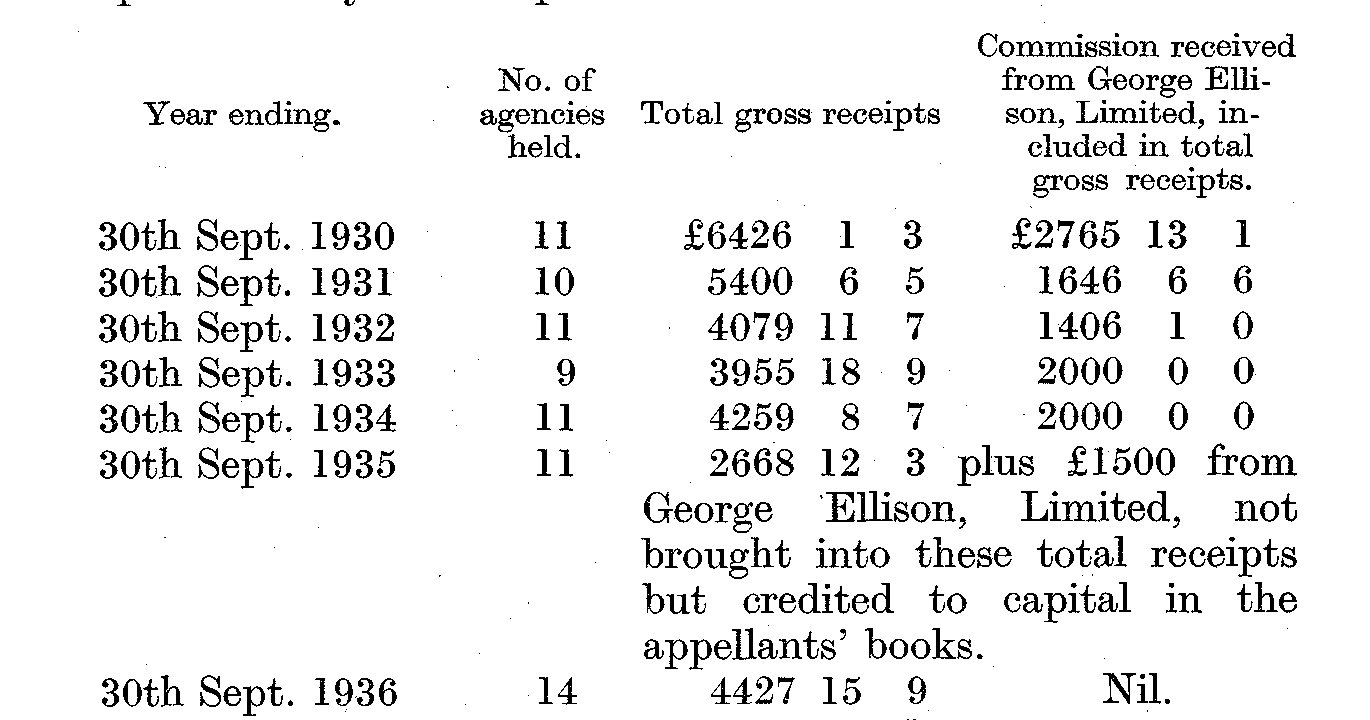

The case set forth:"I. The following facts were admitted or proved:(1) The appellants commenced business in 1914 as manufacturers' agents and engineers. Their business from 1914 up to date has consisted of acting as agents for the sale in Scotland for various manufacturers on a commission basis of such manufacturers' products. (2) In 1914 the appellants had two agencies only, one of which was an agency for the said George Ellison, Limited, electric switch gear manufacturers, Birmingham. The business of the appellants steadily developed and in the last complete seven years the position was as under:

(3) In February 1914 the appellants entered into an agreement with the said George Ellison, Limited, to act as sole representatives in Scotland for the sale there of the products of George Ellison, Limited. This agreement was to subsist for a period of 12 months. The agreement to act as sole sales agents in Scotland for George Ellison, Limited, was renewed for varying periods from time to time thereafter on slightly varying terms up to the 26th September 1923. (4) On the 26th September 1923 a new agreement was

entered into between the appellants and George Ellison, Limited. The new terms were set out in two letters dated the 26th September 1923 as follows:[then followed the letters.2] (5) The appellants acted as selling agents for George Ellison, Limited, on these terms up to the 29th September 1932, when certain variations were made which are set out in the following letter from George Ellison, Limited, to the appellants:

"29th September 1932.

"Messrs Kelsall & Parsons, "

"196 Bath Street,

"Glasgow.

"Dear Sirs, "

"Confirming the conversation to-day with your Mr Parsons it was agreed that you continue to act as our selling representatives

in Scotland. The remuneration for these services to be as follows:A commission of 7 per cent will be paid to you on sales in Scotland up to 30,000 per annum. If the sales exceed 30,000 per annum the commission will be 10 per cent on the amount above 30,000 per annum, with a minimum guaranteed of 2000 per annum payable quarterly. The final settlement of the year's commission to be made in the 4th quarterly payment. A quarterly statement of the invoices to Scotland on which the commission is calculated will be sent to you as before. It is agreed that this arrangement is to be for 3 years from 30th September 1932 providing that your firm consists of the present partners, who are:Mr Kelsall, Mr Parsons, Mr Seedhouse and Mr Helm, and that you will run 3 motor cars and the necessary office establishment. Yours faithfully, For George Ellison, Ltd., (Signed) George Ellison, Governing Director.' (6) In December 1933 George Ellison, Limited, asked the appellants whether they would be willing to take one of the staff of George Ellison, Limited, into their employment to be trained as a sales manager for a branch which George Ellison, Limited, proposed to open in England. At that time George Ellison, Limited, indicated that they would not alter the existing agreement with the appellants for at least 5 to 7 years after the expiry of the then current agreement, which was to run for 3 years from the 30th September 1932. Early in May 1934, however, George Ellison, Limited, approached the appellants with a request that the agency agreement then existing between them and the appellants should be forthwith terminated. The appellants had given the said George Ellison, Limited, no cause for this termination. Negotiations with this end in view then took place between the parties. The appellants would not agree to terminate the agency at once, but they eventually agreed to terminate the agency agreement as from the 1st October 1934, that is, one year before the expiry of the then current contract of agency between the appellants and George Ellison, Limited, on the payment by the latter to the appellants of the sum of 1500. This agreement to cancel the agency contract which the appellants had with George Ellison, Limited, was set forth in the following letter from George Ellison, Limited"George Ellison, Limited.

"26th May 1934.

"Private & Confidential."

"Dear Mr Parsons,

"Thank you for your letter of the 25th inst. I confirm that:1. The existing agreement to run until September 30th 1934. We to pay at the end of each quarter in the usual manner until the above-mentioned date. 2. As compensation for terminating the agreement on September 30th, 1934 instead of September 30th, 1935 we pay you on October 1st 1934, the sum of 1500, this sum to cancel all obligations on either side.

"With kind regards, Yours sincerely, (Signed) George Ellison. (7) The appellants acknowledged the letter last mentioned and confirmed it in the following terms:We are in receipt of your letter of 26th May 1934 confirming the agreement reached between our firm and yours in terms of which you are to pay us 1500 on 1st October next in respect that we have now acquiesced in the cancellation of the previous contract between us. We will continue on the present terms till 30th September. (8) The payment of 1500 by George Ellison, Limited, to the appellants was duly made on the 1st October 1934. It was not credited to the profits of the appellants for the year ending 30th September 1935, but was treated by them as a receipt on account of capital. (9) The sales service of George Ellison, Limited, required the employment of skilled technical people who, in addition to effecting sales, gave technical advice and service to users of their products. In order to perform efficiently their duties as representatives of (inter alios) George Ellison, Limited, the appellants had to build up a considerable technical organisation which could neither be collected nor dispersed at short notice. (10) On the termination of the agency agreement between George Ellison, Limited, and the appellants, the motor cars, provided under the said agreement, were retained by the appellants and used in their business, and of the two salesmen employed under the said agreement one was retained in the employment of the appellants and the other left them and obtained another job. (11) All expenses incurred by the appellants in respect of their sales service for George Ellison, Limited, have been charged in their accounts in arriving at their profits, but no portion of the 1500 received from George Ellison, Limited, has been credited to these profits. (12) The sum of 1500 paid by George Ellison, Limited, was accepted by the appellants in full settlement of any rights or claims they might have under the agency agreement of 29th September 1932 and in respect of its termination one year before it was due to expire."

The case further stated:"III. It was contended on behalf of the appellants, inter alia:(1) That the 1500 received by the appellants from George Ellison, Limited, in the year ending 30th September 1935 was in respect of the surrender by...

To continue reading

Request your trial

-

Anglo-French Exploration Company Ltd v Clayson (Inspector of Taxes)

...cases to which we were referred in this case (as also in the case we decided recently of Wiseburgh v. Domville) of Kelsall parsons & Co. v. Commissioners of Inland Revenue, 21 Tax Cases, page 608, and Commissioners of Inland Revenue v. Fleming & Co. (Machinery) Limited, 33 Tax Cases, Page 5......

-

Anglo-French Exploration Company Ltd v Clayson

...the appeal should be dismissed. VIII. The following cases were referred to :-Kelsall Parsons & Co. v. Commissioners of Inland Revenue,TAX21 T.C. 608Bush, Beach & Gent, Ltd. v. Road, TAX22 T.C. 519Shove v. Dura Manufacturing Co., Ltd., TAX23 T.C. 779Commissioners of Inland Revenue v. Fleming......

-

Wiseburgh v Domville (HM Inspector of Taxes)

...and say "No infallible criterion emerges from a citation of the Case Law. Each case depends upon its own facts". (Kelsall Parsons & Co. V. The Commissioners of Inland Revenue, 21 Tax Cases, page 619). I do not think it necessay to go over the cases which have been cited to us. It is fair to......

-

Higgs v Olivier

...that there is a pertinent observation in one of the cases cited to me, namely Kelsall Parsons & Co. v. Commissioners of Inland Revenue, 21 T.C. 608. The passage I am referring to is at page 619. Lord Normand, then Lord President, said this: "It has been said by Lord Macmillan in Van den "Be......