Reynolds and Gibson v Crompton (HM Inspector of Taxes)

| Jurisdiction | England & Wales |

| Judgment Date | 26 March 1952 |

| Date | 26 March 1952 |

| Court | High Court |

HIGH COURT OF JUSTICE-

COURT OF APPEAL-

HOUSE OF LORDS-

Income Tax, Schedule D, and Profits Tax - Profits of trade - Debt taken over at reduced valuation on change of partnership and subsequently recovered in full - Whether profit assessable.

In September, 1938, a debt of £174,600 due to the Appellant firm (as then constituted) was valued in the firm's books at £124,600, the balance of £50,000 having been transferred to a bad debt reserve account and allowed by deductions in computing profits for Income Tax purposes in previous years. On the retirement of one of the partners, the proviso in Sub-section (1) of Section 32, Finance Act, 1926, was invoked, with the result that the firm was treated for Income Tax purposes as though a new business had been set up with effect from 1st October, 1938. In fixing the consideration payable by the new firm to the old, the debt was valued at its book figure of £124,600. By 30th September, 1945, the firm had recovered £84,114 13s. 10d. of the debt, and had written down the bad debt reserve by re-transferring to profit and loss account sums totalling £40,000 out of the £50,000 previously set aside. A further change in the partnership took place on 30th September, 1945, but the proviso in Sub-section (1) of Section 32, Finance Act, 1926 was not invoked and the firm was therefore treated as one continuing partnership. On 24th December, 1946, the balance of the debt, £90,485 6s. 2d., was paid in full.

The firm was assessed to Income Tax and to Profits Tax on the footing that £50,000, the amount for which deductions had been allowed in past years, should be included in the firm's profits for taxation purposes for the year ended 30th September, 1947. The firm appealed, contending that neither it nor the firm as constituted before the change on 30th September, 1945, carried on the trade of dealing in debts, and that the sums recovered were not receipts of the trade carried on by the firm before and after that change. The Special Commissioners dismissed the appeals and confirmed the assessments. The firm demanded Cases.

Held, that the £50,000 was not a taxable profit of the new trade set up on 1st October, 1938.

Decision in Henry Hall, Ltd. v. Barron, 30 T.C. 45over-ruled.

(1) Reynolds and Gibson v. Crompton (H.M. Inspector of Taxes)

CASE

Stated under the Income Tax Act, 1918, Section 149, by the Commissioners for the Special Purposes of the Income Tax Acts for the opinion of the King's Bench Division of the High Court of Justice.

At a meeting of the Commissioners for the Special Purposes of the Income Tax Acts held on 29th March, 1949 Reynolds and Gibson (hereinafter called "the Appellant firm") appealed against an assessment to Income Tax made upon it for the year ended 5th April, 1949, under the provisions of Case I, Schedule D of the Income Tax Act, 1918.

1. The Appellant firm, a partnership as from time to time differently constituted, has carried on the business of cotton brokers in Liverpool for many years.

2. From 1st October, 1928 to 30th September, 1948 the following table sets out the names of the members of the Appellant firm in which, from time to time, various changes occurred, and are referred to in the table set out below as firm no. 1, no. 2, no. 3, and no. 4 respectively. On the formation of each new firm the assets and liabilities of its predecessor were valued for the purpose of fixing the amount of the consideration to be paid by the new firm to the old and were taken over at the figure so fixed. The assessment appealed against was made upon firm no. 4 which is the Appellant in this case.

1st Oct., 1928 to |

1st Oct., 1933 to |

1st Oct., 1938 to |

1st Oct., 1945 to |

30th Sept., 1933 |

30th Sept., 1938 |

30th Sept., 1941 |

30th Sept., 1948 |

(5 years) |

(5 years) |

(3 years) |

(3 years) |

subsequently |

|||

extended to |

|||

30th Sept., 1944- |

|||

3 years-further |

|||

year at will, i.e., |

|||

30th Sept., 1945 |

|||

Firm No. 1 |

Firm No. 2 |

Firm No. 3 |

Firm No. 4 |

Sir John Shute |

Sir John Shute |

Sir John Shute |

(7)Sir John Shute |

E. B. Orme |

(2)E. B. Orme |

(5)F. R. Verdon |

|

F. R. Verdon |

F. R. Verdon |

(4)F. Reynolds |

Sir John F. R. |

Reynolds, Bt. |

|||

W. J. Walmsley |

(3)W. J. Walmsley |

Sir John F. R. |

|

Reynolds, Bt. |

|||

F. Reynolds |

F. Reynolds |

(6)A. Lightbound |

F. L. Orme |

John F. R. |

Sir John F. R. |

F. L. Orme |

E. R. Orme |

Reynolds |

Reynolds |

||

A. Lightbound |

A. Lightbound |

E. R. Orme |

|

(1)F. L. Orme |

F. L. Orme |

3. The sole question raised by this appeal is whether a sum of £50,000, being the amount of a bad debt reserve, in respect of a debt fully recovered in December, 1946, by firm no. 4 is rightly included in the said assessment by reason of the matters hereinafter set out.

4. About the year 1920 the Appellant firm, as then constituted, in the course of its business supplied cotton to Combined Egyptian Mills, Ltd. (hereinafter referred to as "Combined"). In 1930 a debt, for cotton so supplied, of £200,000 was owing to the Appellant firm, as then constituted, by Combined. The question arose as to how far this debt was good and how far it should be treated as doubtful. In the year ended 30th September, 1930 the Appellant firm, as then constituted, made a reserve of £37,500 against the said debt and in the year to 30th September, 1932 a further reserve of £12,500 making £50,000 in all. The said sums of £37,500 and £12,500 were allowed as deductions in computing its profits and gains for the purposes of Income Tax for the appropriate years of assessment, i.e. 1931-32 and 1933-34.

5. In respect of this debt it was agreed that the Appellant firm as then constituted should draw, and Combined should accept, three-month bills of exchange. The Appellant firm as then constituted took collateral security in the form of a mortgage and the debt was reduced from time to time as the bills were met. In subsequent years it was considered that the said reserve was too drastic and the value of the debt was estimated to be greater than was originally thought to be the case. The said reserve of £50,000 was consequently reduced, the amount of the reductions being recredited to the profit and loss accounts.

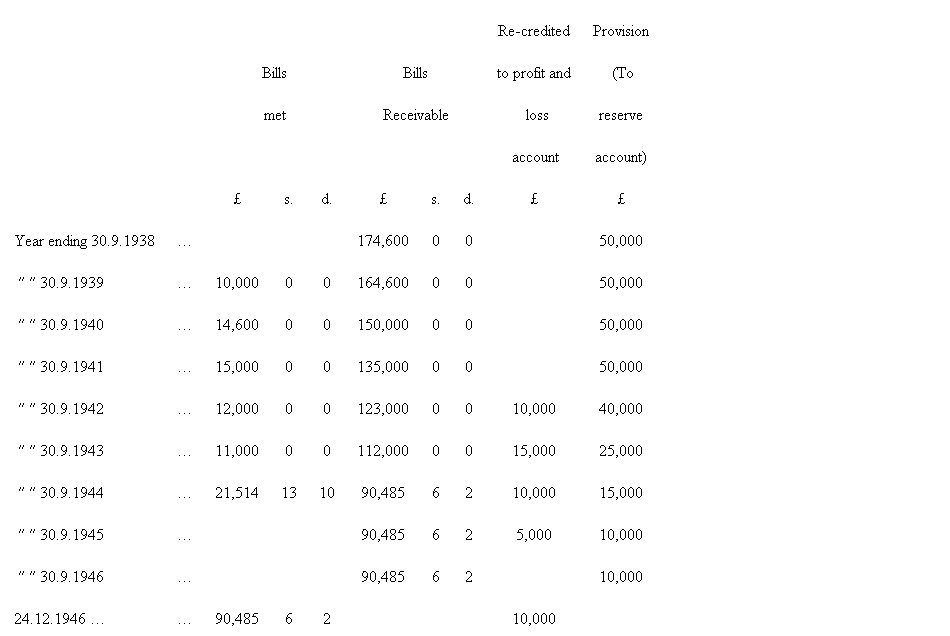

6. The following table sets out the amount of bills of exchange drawn by the Appellant firm as from time to time constituted and accepted by Combined, the said reserve created and subsequently reduced, the amount of the bills honoured by Combined and the amounts of the reserve as reduced credited to the profit and loss accounts of the Appellant firm as then constituted from the year ended 30th September, 1938 to 30th September, 1946.

This table shows that firm no. 3, having been formed on 1st October, 1938, acquired a debt, owing by Combined, from firm no. 2 of £174,600 against which a reserve of £50,000 had been created. The said debt was thus valued at £124,000 at that time. In the years ended 30th September, 1939, 1940, 1941, 1942, 1943 and 1944 firm no. 3 received sums totalling £84,114 13s. 10d. from Combined in respect of the said debt of £174,600. In the years ended 30th September 1942, 1943, 1944 and 1945 firm no. 3 wrote back sums totalling £40,000 from the reserve to its profit and loss accounts. On 24th December, 1946 Combined discharged the balance of the said debt of £174,600 by paying to firm no. 4, which was formed on 1st October, 1945, a sum of £90,485 6s. 2d.

7. Neither firm no. 3 nor firm no. 4 traded in book debts.

8. On the formation of firm no. 3 the proviso to Sub-section (1) of Section 32 of the Finance Act, 1926, was invoked by the partners of firms no. 2 and no. 3. As a consequence firm no. 3 fell to be treated for Income Tax purposes as if a new trade had been set up by it. The said proviso was not invoked on the formation of firm no. 4 which fell to be treated for Income Tax purposes under the provisions of Sub-section (1) of the said Section as between firm no. 3 and itself.

9. It was contended on behalf of the Appellant firm (firm no. 4);

(2) that neither the Appellant firm nor firm no. 3 carried on the trade of dealing in debts and accordingly the sums received by those firms from Combined were not receipts or profits of the trades carried on by them respectively;

(3) that the debt of Combined was never part of the circulating capital of firm no. 3 but was part of the fixed assets of that firm acquired by it on its being constituted;

(4) that the said debt was likewise never part of the circulating capital of the Appellant firm which continued to carry on the trade of firm no. 3 from which the Appellant firm, upon its constitution, acquired the said debt;

(5) alternatively, the said debt was part of the fixed capital assets of the Appellant firm so acquired by it upon its constitution;

(6) the said debt was at no time a book debt of firm no. 3 or of the Appellant firm.

10. It was contended on behalf of the Respondent;

(2) that the receipt by firm no. 3 and firm no. 4 of money owing by Combined Egyptian Mills was not the realisation of capital assets;

(3) that the receipt of the money owing was a part of the ordinary business dealing of firm no. 3 and firm no. 4;

(4) that as no notice under the proviso to Sub-section (1), Section 32 of the Finance Act, 1926, had been given by firm no. 3 and firm no. 4 the businesses carried on by them must, for Income Tax purposes, be regarded as one continuous business carried on since 1st October, 1938;

(5) that the sum of £50,000, the difference between the sum for which the Combined Egyptian Mills debt had been taken over and the amount eventually realised, was properly brought into account in computing the amount of the assessment on firm no. 4.

11. We, the Commissioners, gave our decision as follows.

In September, 1938, firm no. 3 took over from firm no. 2, for £124,600, the debt of £174,600 due from Combined Egyptian Mills. Eventually the...

To continue reading

Request your trial

-

Shop Direct Group v Revenue and Customs Commissioners

... ... of sections 103 and 106 of the Income and Corporation Taxes Act 1988 (" ICTA ") which imposed a charge to corporation ... superseded the decision of the House of Lords in Crompton v Reynolds 33 TC 288 , [1952] 1 All ER 888 ... In ... ...