Strick (HM Inspector of Taxes) v Longsdon

| Jurisdiction | England & Wales |

| Judgment Date | 15 July 1953 |

| Date | 15 July 1953 |

| Court | Chancery Division |

HIGH COURT OF JUSTICE (CHANCERY DIVISION)-

Income Tax, Schedule D - Excess rents - Finance Act, 1940 (3 & 4 Geo. VI, c. 29), Section 15.

In December, 1947, the Respondent granted a lease on certain property. The first half-yearly payment of rent under the lease became due on 6th April, 1948. An assessment was made on him under Case VI of Schedule D for the year 1947-48 in respect of the excess of the rent over the Schedule A assessment on the property.

On appeal the Respondent contended that, under the lease granted in December, 1947, he was not entitled to any rent as respects the year 1947-48 within the meaning of Section 15, Finance Act, 1940. The General Commissioners accepted this contention and discharged the assessment. The Crown demanded a case.

Held, that the Respondent was entitled to rent as respects the year 1947-48.

Stated under Section 149 of the Income Tax Act, 1918, by the Commissioners for the General Purposes of the Income Tax for the Division of Kingston and Elmbridge in the County of Surrey for the opinion of the High Court of Justice.

1. At a meeting of the said Commissioners held on 14th November, 1950, at the Guildhall, Kingston-upon-Thames within the said Division, Captain Edward Henry Longsdon, Royal Navy (retired), (hereinafter called "the Respondent"), appealed against an assessment to Income Tax for the year 1947-48 under Case VI of Schedule D of the Income Tax Act, 1918, in the sum of £204 for excess rent pursuant to Section 15 of the Finance Act, 1940, in respect of lands in the Parish of Barmer in the County of Norfolk, more particularly described in the lease hereinafter mentioned, and owned by the Respondent in fee simple subject to and with the benefit of the said lease.

2. The sole question for our determination was whether, on the facts set out below, the Respondent was liable to be assessed, as aforesaid, under the said Section for the year 1947-48.

-

(a) By a lease dated 13th December, 1947, (hereinafter called "the lease") and made between the Respondent of the one part and Leonard Maurice Mason of the other part.

All those messuages farms lands tenements and hereditaments in the Parish of Barmer in the County of Norfolk

(b)

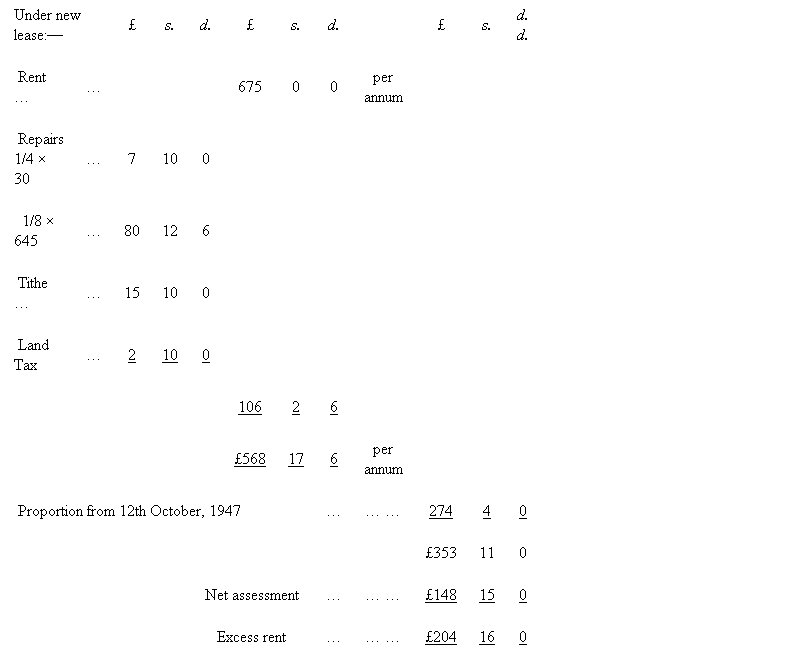

(c) therein more particularly described (hereinafter called "Barmer Farm"), which, however, does not include the farmhouse, were demised to the said Leonard Maurice Mason for the term of four years from 11th October, 1947, at the yearly rent of £675 payable by equal half-yearly payments on 6th April and 11th October in every year, the first payment thereof to be made on 6th April, 1948, and subject to the performance and observance of the covenants on the part of the lessee and the conditions therein contained.

(d) A copy of the counterpart lease is attached hereto marked "A" and forms part of this Case(1).

(e) Immediately prior to the commencement of the term granted by the lease the said Leonard Maurice Mason was tenant to the Respondent of Barmer Farm at an annual rent of £200 under an earlier lease.

(f) The said Leonard Maurice Mason paid no rent under the said lease of 13th December, 1947, prior to 6th April, 1948.

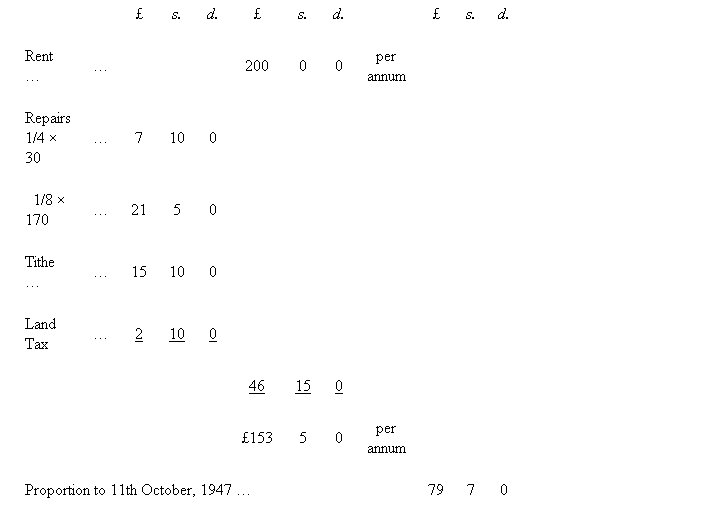

(g) the Respondent was assessed under Schedule A of the Income Tax Act, 1918, in respect of Barmer Farm for the said year 1947-48 on a net annual value of £148 15s. computed as follows:-

| £ | s. | d. | £ | s. | d. | ||

| Gross Annual Value | … | 190 | 10 | 0 | |||

| Less:- | |||||||

| Repairs | … | 23 | 15 | 0 | |||

| Tithe Redemption Annuity | … | 15 | 10 | 0 | |||

| Land Tax | … | 2 | 10 | 0 | |||

| 41 | 15 | 0 | |||||

| Net Annual Value | … | … | … | £148 | 15 | 0 |

(h) This assessment is not under appeal.

(i) The said assessment under Schedule D, Case VI in the sum of £204 for excess rent is computed as follows:-

(j) 6th April, 1947, to 11th October, 1947

(k) Under original lease:-

(l) 12th October, 1947, to 5th April, 1948

4. It was contended on behalf of the Respondent:-

-

(a) that the Respondent was not as respects the year of assessment 1947-48 entitled to any rent payable under the lease within the meaning of Section 15 of the Finance Act, 1940;

-

(b) that for the purpose of Rule 1 of the Miscellaneous Rules applicable to Schedule D (Income Tax Act, 1918) the Respondent in the year of assessment 1947-48 neither received nor was...

To continue reading

Request your trial

-

Trustees of the Tollemache Settled Estates v Coughtrie (HM Inspector of Taxes)

...or "receivable". I do not feel able to accept that view, which is contrary to the view expressed by Vaisey, J., in Strick v.Longsdon, 34 T.C. 528. If the word "entitled" meant "receive", so that you took actual profits, it is clear that that case must have been decided in another way; but, ......

-

Trustees of the Tollemache Settled Estates v Coughtrie (HM Inspector of Taxes)

...or "receivable". I do not feel able to accept that view, which is contrary to the view expressed by Vaisey, J., in Strick v.Longsdon, 34 T.C. 528. If the word "entitled" meant "receive", so that you took actual profits, it is clear that that case must have been decided in another way; but, ......

-

Tollemache Settled Estates Trustees v Coughtrie

... ... the Tollemache Settled Estates) and Coughtrie (Inspector of Taxes) After hearing Counsel, as well on Monday the 16th, ... ...

-

Tollemache Settled Estates Trustees v Coughtrie

...dealt with by direct calculation without a further assessment on Schedule A principles For instance, in the case of Strick v. Longsdon, 34 Tax Cases, 528, the direct figures of the excess rents were used without embarking on further computation (except as to deductions). I sec no reason why......