The Camille and Henry Dreyfus Foundation, Inc. v Commissioners of Inland Revenue

| Jurisdiction | England & Wales |

| Judgment Date | 28 July 1955 |

| Date | 28 July 1955 |

| Court | Chancery Division |

HIGH COURT OF JUSTICE (CHANCERY DIVISION)-

COURT OF APPEAL-

HOUSE OF LORDS-

Income Tax - Exemption - Body of persons established for charitable purposes - Established outside United Kingdom - Income Tax Act, 1918 (8 & 9 Geo. V, c. 40), Section 37 (1) (b).

The Appellant Foundation was incorporated under the Membership Corporations Law of the State of New York, U.S.A., and all its directors were American citizens resident in the U.S.A. Its primary purpose was "to advance the science of chemistry, chemical engineering and related sciences as a means of improving human relations and circumstances throughout the world". The Foundation was entitled to royalties payable by a company resident in the United Kingdom.

The Foundation claimed exemption from Income Tax under Section 37 of the Income Tax Act, 1918, in respect of the royalties, on the ground that it was established for charitable purposes only. The claim was refused by the Commissioners of Inland Revenue. On appeal before the Special Commissioners, the Crown contended that (i) Section 37, Income Tax Act, 1918, applied only to the income of charities established in the United Kingdom, and (ii) the Foundation was not a body established for charitable purposes only. The Special Commissioners upheld the Crown's first contention and dismissed the appeal. They added that if they were wrong on that point they thought that the Foundation was a body of persons established for charitable purposes only. The Foundation demanded a Case.

Held, that the words "any body of persons or trust established for charitable purposes only" in Section 37 (1) (b) are limited to bodies and trusts subject to the jurisdiction of the Courts of the United Kingdom.

Stated under the Income Tax Act, 1952, Section 64, by the Commissioners for the Special Purposes of the Income Tax Acts for the opinion of the Chancery Division of the High Court of Justice.

1. At a meeting of the Commissioners for the Special Purposes of the Income Tax Acts held on 2nd March, 1953, the Camille and Henry Dreyfus Foundation, Inc., hereinafter called "the Foundation", appealed against the

refusal of the Commissioners of Inland Revenue to admit a claim to exemption from Income Tax for the years 1946-47 to 1950-51 inclusive, under the provisions of Section 37 of the Income Tax Act, 1918, and Section 19 (1) of the Finance Act, 1925. The claim was refused by the Commissioners of Inland Revenue for the following reasons:-(a) the Foundation is not established in the United Kingdom and accordingly does not come within Section 37, Income Tax Act, 1918; and

(b) the Foundation is not established for charitable purposes only within the meaning of Section 37.

2. Evidence was given before us by Mr. Lucius Fairchild Crane, a solicitor of the Supreme Court of Judicature in England and a member of the Bar of the State of New York in the United States of America, and by Mr. Henry Blandy Guthrie, a member of the Bar of the State of New York, and a member and a director of the Foundation.

The following facts set out in paragraphs 3 to 7 inclusive of this Case were proved or admitted at the hearing.

3. The Foundation was incorporated on 21st June, 1946, under the Membership Corporations Law of the State of New York and is a membership corporation within the meaning of that law. A copy of the certificate of incorporation of the Foundation, marked "A", is attached to and forms part of this Case(1).

All the directors of the Foundation are American citizens resident in the United States of America.

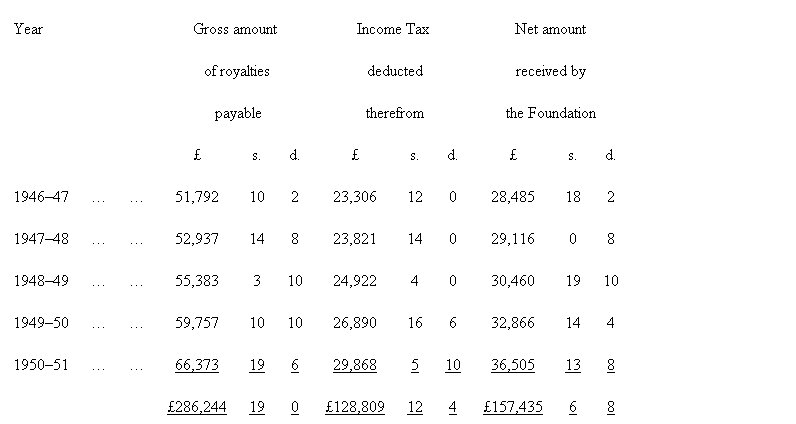

4. On 27th June, 1946, Dr. Camille Dreyfus assigned to the Foundation the benefit of certain agreements under which royalties are payable by British Celanese, Ltd., a company resident in the United Kingdom. By virtue of the assignment the Foundation received the following royalties from British Celanese, Ltd., from which Income Tax was deducted as shown:-

-

(a) The statutory law (other than special or private Acts) of the State of New York is to be found in a series of general laws of which the Membership Corporations Law is one. In the case of the Membership Corporations Law as in the case of other general laws providing for the formation of other types of corporation, a corporation to be formed there-under can only derive its purposes and powers from the particular general law under which it is formed. It cannot arrogate to itself, by clauses in its

certificate of incorporation, purposes and powers not authorised by the Statute. If such unauthorised powers or purposes are inserted in the certificate of incorporation they do not constitute part of the charter of the corporation but are rejected as surplusage and extraneous matter. If the articles of association contain the matters required by the Statute and also contain additional matters, the former are sufficient to sustain the charter, and the additional matter does not vitiate the legitimate part of the articles, but the additional matter is disregarded by the law as though it had not been written. (b) Section 2 of the Membership Corporations Law defines a membership corporation as

a corporation not organised for pecuniary profit, incorporated under this chapter, or under any law repealed by this chapter; but unless hereinafter specifically provided does not include a membership corporation created by a special law or a corporation subject to any of the provisions of the insurance law.

(c) Section 10 of that Law provides that:-

Five or more persons may become a membership corporation for any lawful purpose, or for two or more such purposes of a kindred or incidental nature, except a purpose for which a corporation may be created under any general law other than this chapter.

(d) To be valid, therefore, all the purposes of a corporation formed under the Membership Corporations Law must be of a kindred or incidental nature.

(e) Clause 2 of the certificate of incorporation (exhibit A(1)) defined the primary purpose of the Foundation as being

a. To advance the science of chemistry, chemical engineering and related sciences as a means of improving human relations and circumstances throughout the world.

(f) Sub-clauses (1) and (2) of clause 2a recite the methods of accomplishing that primary purpose by the performance of acts

in such fields of science

(g) and

relating to such fields of science.

(h) Sub-clause (3) of that clause refers to further methods and repeats the words

science of chemistry, chemical engineering and related sciences.

(i) Clause 2b states as further purposes of the Foundation:-

To promote any other scientific, educational or charitable purposes.

The purposes there stated are not of a nature kindred or incidental to the primary purpose set out in clause 2a. They are accordingly not authorized by Section 10 of the Membership Corporations Law and are void and to be treated as surplusage. The use of the word "other" negatives the idea that the purposes in clause 2b are of a nature kindred or incidental to those set out in clause 2a. The "other scientific…purposes" referred to could comprise any branch of science, e.g., medicine or anthropology, quite distinct from and unrelated to "the science of chemistry, chemical engineering and related sciences". Moreover, "other…educational or charitable purposes" are in no sense kindred to or incidental to the "science of chemistry, chemical engineering and related sciences", since they might well comprise purposes which had nothing whatever to do with those sciences.

The certificate of incorporation, apart from the contents of clause 2b which are void, is not otherwise affected and remains valid.

6. During the material years the Foundation was exempt from American Federal Income Tax under the provisions of Section 101 (6) of the Inland

Revenue Code on the ground that the Foundation was organised and operated exclusively for educational, scientific and charitable purposes.7. During the material period, viz. from 25th June, 1946, to 31st December, 1950, the Foundation invested the sums received by way of royalties from British Celanese, Ltd. Out of its income from investments the Foundation made grants to various institutions to be applied for the advancement of chemistry and chemical engineering. A summary of the contributions so made, marked "B", is attached to and forms part of this Case(1).

8. The following documents, which were produced to us, are attached and may be referred to(1).

(a) A copy of the by-laws of the Foundation.

(b) A copy of the assignment dated 27th June, 1946, from Camille Dreyfus to the Foundation.

(c) A statement of the cash receipts and disbursements of the Foundation for the period from 25th June, 1946, to 31st December, 1951.

9. It was contended on behalf of the Foundation that upon a true construction of Section 37, Income Tax Act, 1918, the Foundation, being a body of persons established for charitable purposes only, is entitled to exemption from tax thereunder notwithstanding that it was so established outside the United Kingdom.

10. It was contended on behalf of the Crown:-

(a) that on the authority of the decision in Commissioners of Inland Revenue v. Gull, 21 T.C. 374, the Foundation is precluded from exemption from tax under Section 37, Income Tax Act, 1918, because it is not a body of persons established in the United Kingdom; and

(b) that if the Foundation is not so precluded it is not a body established for charitable purposes only within the meaning of the said Section 37.

11. We, the Commissioners who heard the Case, gave our decision as follows:-

1. There are two points which require determination, viz. (a)whether the Foundation not being a body of persons established in the United Kingdom is thereby precluded from relief under Section 37; and (b) if the Foundation is not so precluded, whether it is a body of persons established for charitable purposes only.

2. As regards the first...

To continue reading

Request your trial

-

Revenue Commissioners v Sisters of Charity

... ... ACT 1918 S37 FINANCE ACT 1921 CAMILLE & HENRY DREYFUS FOUNDATION INC V COMMISSIONERS OF INLAND REVENUE 1955 36 TC 126 COMMISSIONERS OF ... ...