Gordon

| Jurisdiction | UK Non-devolved |

| Judgment Date | 29 November 2022 |

| Neutral Citation | [2022] UKFTT 437 |

| Court | First-tier Tribunal (General Regulatory Chamber) |

[2022] UKFTT 437 (GRC)

Tribunal Judge Sophie Buckley

First-tier Tribunal (General Regulatory Chamber, Information Rights)

Freedom of information request – Whether HMRC entitled to refuse request to name taxpayer even though already in public domain – Yes – Appeal Dismissed – Freedom of Information Act 2000 (FOIA 2000), s. 44(1)(a), Commissioners for Revenue and Customs Act 2005 (CRCA 2005), s. 18(1), 19(2) and 23.

In Gordon v Information Commissioner & Anor [2022] UKFTT 437 (GRC), the First-tier Tribunal General Regulatory Chamber dismissed a barrister’s appeal against the Information Commissioner’s decision that HMRC were entitled to withhold information under the Freedom of Information Act 2000 (FOIA 2000).

The appellant (Mr Gordon) had received an email from a senior HMRC official about disguised remuneration and the loan charge. This included the sentence “Are we just hoping [redacted] will put people off?”. Mr Gordon had asked HMRC on what basis the word(s) and/or number(s) had been redacted and asked that the redacted word(s) and/or number(s) be supplied. HMRC refused on the basis that under the Commissioners for Revenue and Customs Act 2005 (CRCA 2005), s. 23, the information was exempt from disclosure under FOIA 2000, s. 44(1)(a), because the information was prohibited from disclosure by CRCA 2005, s. 18(1), as it was held by them in connection with one of their functions, and would have enabled the person to whom the information related to be deduced.

Mr Gordon asked HMRC to confirm that the redacted information was the name of a taxpayer, whether that taxpayer was or had been in litigation with HMRC and whether there had been any published decisions in the course of that litigation. HMRC again refused to provide the information.

Mr Gordon referred the matter to the Information Commissioner, and in decision notice IC-125944-L6R0, the Commissioner decided that HMRC were entitled to refuse to provide the information.

Mr Gordon appealed to the First-tier Tribunal General Regulatory Chamber on the grounds that the Commissioner was wrong to conclude that FOIA 2000, s. 44(1) applied by virtue of CRCA 2005, s. 23 and 18(1), where the withheld information was the name of a Supreme Court case and not the name of a taxpayer.

The tribunal found that:

- the requested information was the redacted section of the email, not the whole email;

- while the name of a reported Supreme Court case would be in the public domain, HMRC would have acquired the name as a result of the their litigation functions in respect of the taxpayer in question and therefore the requested information was revenue and customs information relating to a person;

- the disclosure of the information was prohibited by CRCA 2005, s. 18(1) because it was held by HMRC in connection with their function; and

- disclosure would have specified the identity of the person to whom the information related or would have enabled the identity of that person to be deduced.

The tribunal concluded that the disclosure of the information was prohibited.

The tribunal had sympathy with the argument that disclosing the name of a reported case would not breach the principle of taxpayer confidentiality, but found that it had no scope other than to apply the statutory test of whether the information was held by HMRC in connection with a function of HMRC. Albeit that in the tribunal’s view this was not what the drafters of the legislation had intended.

For commentary on HMRC and freedom of information, see In-Depth at .

Comment by Meg Wilson, Lead Tax Writer, Croner-i Ltd.

[1] This is an appeal against the Commissioner's decision notice IC-125944-L6R0 of 18 May 2022 which held that HMRC was entitled to rely on s 44(1)(a) FOIA (prohibition on disclosure) to refuse the request. The Commissioner did not require the public authority to take any steps.

[2] This appeal concerns a request made on 21 July 2021 and a supplementary request made on 22 July 2021.

[3] Mr. Gordon made the following request to HMRC on 22 July 2021:

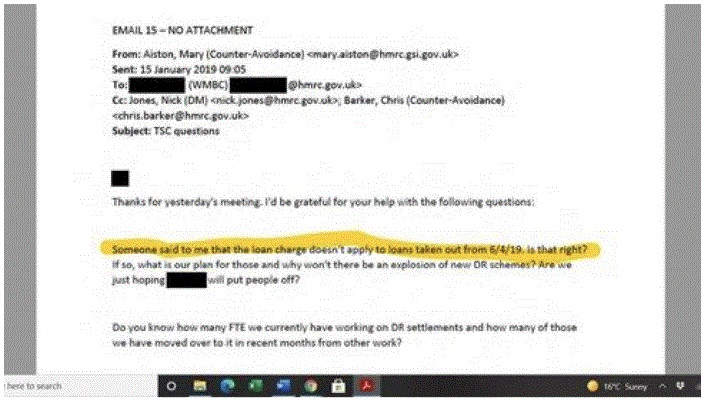

Ms Mary Aiston sent an e-mail dated 15 January 2019, timed at 09.05. Its subject was “TSC Questions.” A screen shot of that e-mail is shown below.

The second substantive paragraph contains the question “If so, what is our plan for those and why won't there be an explosion of new DR schemes?” Immediately after that question, there is a sentence with word(s) and/or number(s) between “hoping” and “will” redacted.

- Please confirm that this redaction is still appropriate.

- If so, please identify the statutory basis for such redaction.

- If the redaction is no longer considered appropriate, please supply the word(s) and/or number(s) previously redacted.

Please note that I have previously raised this informally with the Press Office but they have not responded to this request. Hence my formal request.

[4] HMRC responded on 22 July 2021 refusing to provide the information under s 44(1)(a) FOIA, relying on s 23 of the Commissioners for Revenue and Customs Act 2005 (CRCA) which provides that information relating to a person, the disclosure of which is prohibited by s 18(1) CRCA, is exempt information by virtue of s 44(1)(a) FOIA if its disclosure would enable the identity of such a person to be deduced.

[5] Mr. Gordon submitted the following supplemental request on 22 July 2021:

Are you able please to confirm:

- That the omitted information is the name of a taxpayer

- If so, that that taxpayer was or had been in the course of litigation with HMRC in relation to related matters.

- If the answer to 2 is yes, whether there had been any published decisions in the course of that litigation by 15 January 2019

- If the answer to 2 is yes but the answer to 3 is no, whether there have been any published decisions in the course of that litigation since 15 January 2019?

Any other information you are able to provide that clarifies the nature of the redacted information (for example a description of any words other than the taxpayer's name) would be most appreciated.

[6] HMRC replied on 23 July 2021 refusing to provide the information under s 44(1)(a) FOIA on the same grounds.

[7] Mr. Gordon requested an internal review on 23 July 2021. HMRC upheld its decision on internal review on 23 August 2021.

[8] Mr Gordon referred the matter to the Commissioner on 24 August 2021.

[9] In a decision notice dated 18 May 2022 the Commissioner decided that HMRC was entitled to rely on s 44(1)(a) FOIA.

[10] The Commissioner concluded that the information was held by HMRC in connection with its function of assessing and collecting tax. It therefore fell under section 18(1) CRCA and is prohibited from disclosure.

[11] Section 23(1) CRCA designates information as exempt from disclosure under section 44(1)(a) FOIA if its disclosure would identify the person to whom it relates or would enable the identity of such a person to be deduced. The term “person” includes both natural and legal persons and therefore includes entities such as companies, and charities as well as individuals.

[12] The Commissioner considered Mr. Gordon's arguments that there is no duty of confidentiality as it can reasonably be inferred that the redacted information is the name of a case that went to the Supreme Court. The Commissioner was not persuaded that this was a strong enough argument to override the specific sections of the CRCA which clearly state that such information is prohibited from disclosure.

[13] The ground of appeal is that the Commissioner was wrong to conclude that s 44(1) applied by virtue of s 23 and 18(1) CRCA where the withheld information is the name of a Supreme Court case and not the name of a taxpayer.

[14] We took account of oral and written submissions from HMRC and Mr Gordon.

[15] HMRC submits that the provisions in CRCA put on a statutory footing the longstanding principle of taxpayer confidentiality. HMRC's position is that section 18(1) prevents disclosure of any information it holds in connection with its functions – meaning all of that information (even information otherwise in the public domain) is subject to the principle of taxpayer confidentiality. Section 23 makes a limited exception to the principle of taxpayer confidentiality for FOIA purposes but deliberately excludes any information relating to an identifiable individual.

[16] Without confirming or denying Mr. Gordon's supposition that the requested information related to a “published case”, HMRC submits that:

16.1. disclosure of the name of a published case was information protected by sections 18 and 23 of the CRCA; and

16.2. no allowance is made under section 23 for information that has entered the public domain.

[17] The name of a published case (or any information capable of revealing the name of that case) to which HMRC was a party is information “about, acquired as a result of, or held in connection with” HMRC's tax litigation function. The name of the other party (as it appears in the reported name of the case) is information “in respect of” that person. Therefore the name of a published case is “revenue and customs information relating to a person” within the meaning of section 19(2) of the CRCA.

[18] The name of a published case is “held by the Revenue and Customs in connection with a function of the Revenue and Customs” as a result of HMRC's assessment and collection of tax from the taxpayer and therefore was information to which s 18 applied. The fact that the name of that taxpayer may have entered the public domain does not mean that s 18 ceases to apply. S 18 applies to any information held by HMRC in connection with its functions.

[19] Disclosure of the name of a published case “would specify the identity of the person to whom it relates”.

[20] It follows...

To continue reading

Request your trial