Kellogg Brown and Root Holdings Ltd v HM Revenue and Customs

| Jurisdiction | England & Wales |

| Judge | Lord Justice Longmore,Lady Justice Smith |

| Judgment Date | 24 February 2010 |

| Neutral Citation | [2010] EWCA Civ 118 |

| Docket Number | Case No: A3/2009/0935 |

| Court | Court of Appeal (Civil Division) |

| Date | 24 February 2010 |

[2010] EWCA Civ 118

COURT OF APPEAL (CIVIL DIVISION)

ON APPEAL FROM THE HIGH COURT OF JUSTICE

(CHANCERY DIVISION)

The Rt Hon the Chancellor of the High Court

Before: The Master of the Rolls

Lord Justice Longmore

and

Lady Justice Smith

Case No: A3/2009/0935

Mr John Gardiner QC and Mr Philip Walford (instructed by Norton Rose LLP) for the Appellant

Mr Rupert Baldry (instructed by the Solicitor for HM Revenue and Customs) for the Respondents

Hearing date: 2 February 2010

Lord Neuberger MR:

This is an appeal brought by a taxpayer against a decision of Sir Andrew Morritt C, upholding a decision of the Special Commissioner, Dr John Avery Jones CBE. The appeal raises two issues of construction; the first centres on the meaning of the word “group” in section 286(5)(b) of the Taxation of Chargeable Gains Act 1992 (“the 1992 Act”), and the second concerns the ambit of section 416(2) of the Income and Corporation Taxes Act 1988 (“the 1988 Act”). By a respondent's notice Her Majesty's Commissioners of Revenue and Customs (“HMRC”) raise a further issue which principally turns on the ambit of section 28 of the 1992 Act.

The Special Commissioner had dismissed an appeal against an amendment made by HMRC to the appellant's tax return, disallowing a claim to deduct a capital loss of £14,867,445 against chargeable gains in its accounting period ended 31 December 2000. He held that the capital loss was not available to be so deducted on the basis that it was a loss between connected persons falling within section 18(3) of the 1992 Act, which provides that a loss arising on a disposal between connected persons can only be deducted from chargeable gains arising on other disposals between the same connected persons. For similar, if not identical, reasons, the Chancellor agreed.

A summary of the relevant facts

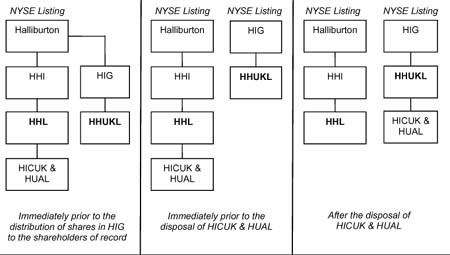

The appellant, Kellogg Brown & Root Holdings (UK) Ltd, formerly known as Halliburton Holdings Ltd (“HHL”), is a United Kingdom incorporated and tax resident company. HHL was a directly wholly-owned subsidiary of Halliburton Holdings Inc (“HHI”), which and was itself a wholly-owned subsidiary of Halliburton Company (“Halliburton”), a United States-based multinational company publicly listed on the New York Stock Exchange carrying on engineering and other operations worldwide. HHL had two insurance subsidiaries, Highlands Insurance Company (UK) Limited (“HICUK”) and Highlands Underwriting Agents Limited (“HUAL”).

Halliburton had a number of wholly owned subsidiaries apart from HHI. Only one of those is relevant for present purposes, namely Highlands Insurance Group Inc (“HIG”). During 1995, Halliburton decided to divest itself of its global insurance division by floating off HIG, which would thus become the ultimate parent company of all the insurance companies then in the Halliburton group. In the UK, the intention was that the shares in the HICUK and HUAL would be transferred to a newly incorporated UK company called Highlands Holdings (UK) Limited (“HHUKL”), which was formed as a subsidiary of HIG, the company which was to be the new independent US parent company of the insurance division.

The floating off of HIG was governed by a “Distribution Agreement” dated 10 October 1995. Pursuant to that agreement, at 8.30 am (Houston time) on 23 January 1996, Halliburton's shares in HIG were distributed to the shareholders of Halliburton as at 4 January 1996, which was the record date for the distribution. A little later on 23 January 1996, at 8.45 am (Houston time), pursuant to a “Disposal Agreement” dated 18 January 1996, HHL made a disposal of the entire share capital of its two insurance subsidiaries, HICUK and HUAL, to HHUKL. Under the terms of the Disposal Agreement, it was specifically provided that the obligation to complete the disposal of HICUK and HUAL was “conditional on … the Distribution [of the shares in HIG] pursuant to the Distribution Agreement”. The capital loss that was claimed, which HMRC have disallowed, arose on HHL's disposal to HHUKL of the share capital in HICUK and HUAL.

The following table, provided by counsel for HHL, helpfully illustrates the position:

Halliburton's shares were widely held and traded daily. On 31 December 1995, it had approximately 16,400 shareholders of record, and only one of those shareholders, who owned 5.95 per cent, had more than 5 per cent of the shares. The Special Commissioner found that on 23 January 1996 the shareholders of Halliburton Company and of HIG were not identical (there appears to have been a difference of about 16 per cent, presumably reflecting transactions in Halliburton shares effected between 4 January and 23 January 1996). However, unsurprisingly in the circumstances I have described, he also concluded that it would be possible to identify a collection of shareholders who owned the greater part of the share capital of both companies.

The relevant legislation

As its name indicates, the 1992 Act is concerned with the computation of, and assessment of liability for tax on, capital gains. The cross-appeal raises issues as to the time at which transactions occur, or are deemed to occur. This requires one to consider the effect of section 28 of the 1992 Act (“section 28”), which is entitled “Time of disposal and acquisition where asset disposed of under contract”, and provides as follows:

“(1) Subject to section 22(2), and subsection (2) below, where an asset is disposed of and acquired under a contract the time at which the disposal and acquisition is made is the time the contract is made (and not, if different, the time at which the asset is conveyed or transferred).

(2) If the contract is conditional (and in particular if it is conditional on the exercise of an option) the time at which the disposal and acquisition is made is the time when the condition is satisfied.”

In general, a taxpayer can set off against his liability for tax on capital gains any capital loss which he has suffered. However, as is of central importance on this appeal, this right is cut down by section 18 of the 1992 Act (“section 18”), which is concerned with “Transactions between connected persons”, and is in the following terms:

“(1) This section shall apply where a person acquires an asset and the person making the disposal is connected with him.

(2) Without prejudice to the generality of section 17(1) the person acquiring the asset and the person making the disposal shall be treated as parties to a transaction otherwise than by way of a bargain made at arm's length.

(3) Subject to subsection (4) below, if on the disposal a loss accrues to the person making the disposal, it shall not be deductible except from a chargeable gain accruing to him on some other disposal of an asset to the person acquiring the asset mentioned in subsection (1) above, being a disposal made at a time when they are connected persons.”

The reference to “connected persons” at the end of section 18(3) takes one to section 286 of the 1992 Act (“section 286”), which is headed “Connected persons: interpretation”, and, so far as relevant, provides as follows:

“(1) Any question whether a person is connected with another shall for the purposes of this Act be determined in accordance with the following subsections of this section (any provision that one person is connected with another being taken to mean that they are connected with one another). ….

(5) A company is connected with another company—

(a) if the same person has control of both, or a person has control of one and persons connected with him, or he and persons connected with him, have control of the other, or

(b) if a group of 2 or more persons has control of each company, and the groups either consist of the same persons or could be regarded as consisting of the same persons by treating (in one or more cases) a member of either group as replaced by a person with whom he is connected.

(6) A company is connected with another person, if that person has control of it or if that person and persons connected with him together have control of it.

(7) Any two or more persons acting together to secure or exercise control of a company shall be treated in relation to that company as connected with one another and with any person acting on the directions of any of them to secure or exercise control of the company.

(8) In this section “relative” means brother, sister, ancestor or lineal descendant.”

The reference to “control” in section 286 of the 1992 Act is expanded in section 288(1) of that Act (“section 288(1)”), which states that: “unless the context otherwise requires …‘control’ shall be construed in accordance with section 416 of the [1988] Act”. Section 416 of the 1988 Act (“section 416”) is one of the provisions in Part XI of that Act which is concerned with “close companies”, that is, companies which are controlled by a few individuals who would be able, in the absence of those provisions, to accumulate income in such a company without having to pay personal (as opposed to corporation) tax on it. In very general terms, a company cannot be “close”, if, under section 414, it is not controlled by fewer than six people, or, under section 415, if at least 35% of its shares are quoted.

Section 416 is headed “Meaning of ‘associated company’ and ‘control’”, and is in these terms, so far as relevant:

“…(2) For the purposes of this Part, a person shall be taken to have control of a company if he exercises, or is able to...

To continue reading

Request your trial

-

UBS AG v HMRC

...to the relatively recent decision of the Court of Appeal in Kellogg Brown & Root Holdings (UK) Ltd v Revenue and Customs Commissioners [2010] EWCA Civ 118, [2010] STC 925, where Lord Neuberger MR (with whose judgment Longmore and Smith LJJ agreed) referred to the observations of Lord Hoffma......

-

DB Group Services Ltd v HMRC

...to the relatively recent decision of the Court of Appeal in Kellogg Brown & Root Holdings (UK) Ltd v Revenue and Customs Commissioners [2010] EWCA Civ 118, [2010] STC 925, where Lord Neuberger MR (with whose judgment Longmore and Smith LJJ agreed) referred to the observations of Lord Hoffma......

-

UBS v Revenue and Customs Commissioners; Deutsche Bank Group Services (UK) Ltd v Revenue and Customs Commissioners

...4; [2010] BTC 112; [2010] 1 WLR 497 IR Commrs v CrossmanELR [1937] AC 26 Kellogg Brown & Root Holdings (UK) Ltd v R & C CommrsUNKTAX [2010] EWCA Civ 118; [2010] BTC 250 Lynall v IR CommrsELRTAX [1972] AC 680; (1971) 47 TC 375 MacDonald v Dextra Accessories LtdUNKTAX [2005] UKHL 47; [2005] B......

-

UBS AG and DB Group Services (UK) Limited v The Commissioners for HM Revenue and Customs

...to the relatively recent decision of the Court of Appeal in Kellogg Brown & Root Holdings (UK) Ltd v Revenue and Customs Commissioners [2010] EWCA Civ 118, [2010] STC 925, where Lord Neuberger MR (with whose judgment Longmore and Smith LJJ agreed) referred to the observations of Lord Hoffma......